Amazon Just Changed How You Get Paid. Here's What It Costs You.

Amazon just fundamentally changed how they hold your money. Not how much they pay you — but when they release it. And the difference is bigger than most sellers realize.

The Real Story: Your Balance Used to Go to Zero

Under the old system, when Amazon paid you, your seller balance went to zero. Everything was released. Money flowed through your account like a pipe — it came in, it went out, nothing stayed behind.

With DD+7, that changes completely. Amazon now holds every order individually in “Deferred Transactions” until 7 days after delivery confirmation. This creates a permanent pool of your money that never empties. As old orders clear out, new ones take their place. Your balance never goes to zero again.

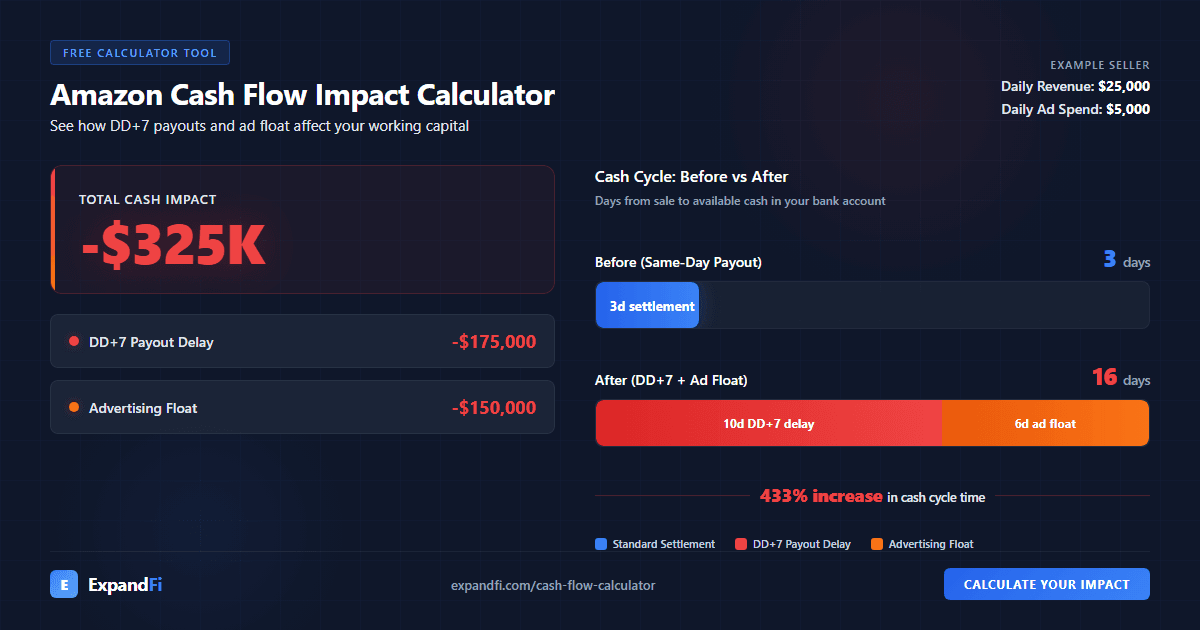

We analyzed settlement data across ExpandFi merchants and tracked actual orders from purchase date through to the deposit date when money hit the bank. The median order-to-bank time before DD+7 was ~7 days. After DD+7, it’s ~9 days. The timing shift is modest — but the permanent reserve is massive.

If your daily payout is $25,000 and Amazon holds ~9 days at all times, that’s $225,000 permanently sitting in Amazon’s Deferred Transactions pool. Money that used to be in your bank account.

DD+7 Didn’t Hit Everyone on March 12

Amazon officially set March 12, 2026 as the DD+7 deadline, but many accounts were migrated much earlier. We found accounts that shifted to DD+7 hold patterns in late 2024 — five months before the official deadline. If your payout timing didn’t change in March, your account was likely already transitioned.

The key insight: how often you get paid (daily, weekly, biweekly) is different from how long each order’s money is held. You can press the “Request Payment” button every day, but you can only pull out what’s “Available” — and Deferred funds aren’t available. Frequent payouts don’t help if the money is still in the hold period.

The Ad Payment Change (April 15, 2026)

Amazon announced that ad costs will be deducted directly from your seller proceeds instead of charging your credit card. This is not rolling out to all accounts — Amazon is applying it selectively, and the full scope is unclear.

If it applies to you, you lose the ~30-day credit card float. For a seller spending $5,000/day on ads, that’s $150,000 in free short-term financing that disappears.

However, there are two potential ways to keep your float:

- Keep a low seller balance. Amazon confirmed that if your balance is insufficient to cover ad charges, they will still charge your credit card as a backup. Requesting frequent payouts to keep your balance low may preserve this fallback.

- Switch to Pay by Invoice. Amazon offers Net 30 payment terms via wire transfer. This could provide similar or better cash flow flexibility compared to credit card billing. Check Advertising > Payment Methods in Seller Central.

Total Cash Amazon Holds

Adding it up for a seller with $25,000/day in payouts and $5,000/day in ad spend:

| Component | Cash Held |

|---|---|

| Permanent Reserve (Deferred Transactions) | $225,000 |

| Ad Float Lost (if change applies) | $150,000 |

| Total Cash Amazon Holds | $375,000 |

That’s $375,000 of your cash that Amazon holds at any given time instead of it being in your bank account. Your profit is unchanged — but your available cash is permanently reduced.

How We Verified This

We didn’t estimate. We tracked actual orders from purchase date through settlement reports to the deposit date (when money actually lands in your bank). Not the “posted date” (which is just Amazon’s internal ledger recording).

Across our merchants, we measured tens of thousands of orders before and after March 12. The results: payout timing shifted modestly (7 to 9 days median), but the permanent reserve is the real story. One merchant went from $0 in reserves to over $1 million permanently held in Deferred Transactions.

What You Can Do

- Understand your permanent reserve. Check your Seller Central Payments Dashboard > Deferred Transactions. That number is your new baseline — it won’t go to zero.

- Plan for the ad float change. If you receive a notification, consider the low-balance strategy or Pay by Invoice.

- Secure a line of credit now — before you need it. Easier to get when your cash position is strong.

- Hold off on distributions until your cash rebuilds to the new baseline.

- Negotiate Net 60 with suppliers to offset the cash cycle extension.

Calculate Your Impact

We built a free Amazon Cash Flow Impact Calculator that shows how much cash Amazon holds from your business. Enter your daily payout and daily ad spend — that’s it.

If you’re an ExpandFi customer, we calculate this automatically from your actual settlement data — including your real deposit dates, payout frequency, and reserve history. No estimates.

See how much cash Amazon holds from your business →

Open the CalculatorKnow your numbers. Plan ahead. And check your Deferred Transactions balance — that’s the number that tells the real story.